Finding yourself abroad without travel insurance can be stressful. Maybe you forgot to buy a policy before departing, thought your credit card covered you, or your plan has expired.

Securing travel insurance already overseas is essential for your peace of mind. But can you purchase travel insurance after leaving home? Yes, you have options.

Let’s explore how to protect yourself while traveling and what to consider when choosing a policy.

Can You Buy Travel Insurance After Leaving Home?

Absolutely! Many travelers find themselves in this situation, and insurance companies now offer solutions. You can buy travel insurance already overseas, though not all insurers provide this option.

Certain insurers specialize in policies for travelers who have already left home or are staying abroad longer. Most traditional travel insurance plans require you to buy coverage before you depart. However, some companies now offer travel insurance already overseas to meet the needs of travelers who are already on the road.

A recent survey shows that nearly 25% of travelers have bought or considered buying travel insurance while already abroad. This trend highlights the need for flexible options that accommodate unexpected travel changes.

Options for Travel Insurance Already Overseas

When looking for insurance plans suitable for your situation, seek companies that cater to travelers already abroad. Some notable insurance companies offering this type of coverage include:

- World Nomads: Provides flexible travel insurance plans that you can purchase from anywhere, even after starting your trip. You can extend policies online, which is convenient for long-term travelers.

- SafetyWing: Offers affordable travel medical insurance designed for digital nomads and long-term travelers. You can start your policy while abroad, with automatic monthly payments.

- IMG Global: Features various international medical insurance plans that fit individuals, families, and groups. Their plans include comprehensive medical coverage, including emergency evacuation.

- Allianz Global Assistance: While some plans require purchase before departure, they offer options that may cover travelers already overseas. Always review specific terms.

Please note that policy terms and conditions vary between providers. It’s important to read the fine print to understand what is covered and what isn’t.

Coverage Details: What Does Overseas Travel Insurance Include?

Travel insurance cover can be extensive, even when bought after departure. Typical inclusions are:

- Medical Expenses: Covers unexpected illness or injury requiring medical care, including hospital stays, doctor visits, and sometimes dental emergencies.

- Emergency Evacuation and Return: Pays for emergency transportation to the nearest appropriate medical facility or returning you to your home country if needed.

Trip Interruption or Cancellation: Gives you your money back if your trip is canceled or cut short because you are sick or have a family emergency.

- Lost, Stolen, or Damaged Property: Pays you for personal items like luggage, electronics, and passports that are lost, stolen, or damaged.

- Adventure Activities Coverage: If you plan to engage in activities like skiing, diving, or hiking, ensure your policy covers adventure activities.

- Personal Liability: Protects you if you’re held legally responsible for injury to a third party or damage to their property.

However, when purchasing travel insurance already overseas, be aware of potential limitations:

- Waiting Periods: Some policies require a waiting period (e.g., 48-72 hours) before coverage starts, especially for medical expenses.

- Pre-Existing Conditions: Most policies exclude coverage for pre-existing medical conditions or require you to buy additional coverage.

- Reduced Benefits: Certain benefits might be limited compared to policies bought before departure.

Example:

Imagine you’re trekking in Nepal and hurt your ankle badly. Without travel insurance, medical care and emergency transportation could cost thousands. But with a comprehensive policy, these expenses would be covered, ensuring you receive the necessary treatment without financial strain.

Key Considerations: Pre-Existing Conditions and Waiting Periods

Pre-Existing Conditions

A pre-existing condition is any illness or injury that existed before your insurance policy starts. When buying travel insurance already overseas, coverage for pre-existing conditions is crucial. Most standard policies exclude these conditions, meaning related medical expenses won’t be covered.

Some insurers offer waivers or additional coverage for pre-existing conditions, but there may be specific requirements:

- Stable Condition Clause: The condition must have been stable (no changes in medication or treatment) for a certain period before the policy starts.

- Additional Premium: You might need to pay extra to include coverage for pre-existing conditions.

- Documentation: Providing medical records or a doctor’s statement may be necessary.

Disclose any existing medical issues when purchasing your policy to avoid complications during a claim.

Waiting Periods

Waiting periods are common when buying travel insurance after departure. This is the time that must pass before certain coverages become active. For example:

- Medical coverage typically has a 48-72 hour waiting period for claims, so purchasing insurance after getting sick or injured won’t cover those expenses.

- Trip Cancellation/Interruption: Coverage might not apply to events that were foreseeable before purchasing the policy.

Understanding these waiting periods is crucial to ensure you have the coverage you need when you need it.

Choosing the Best Travel Insurance When Already Abroad

Selecting the best travel insurance when already abroad requires careful research and consideration:

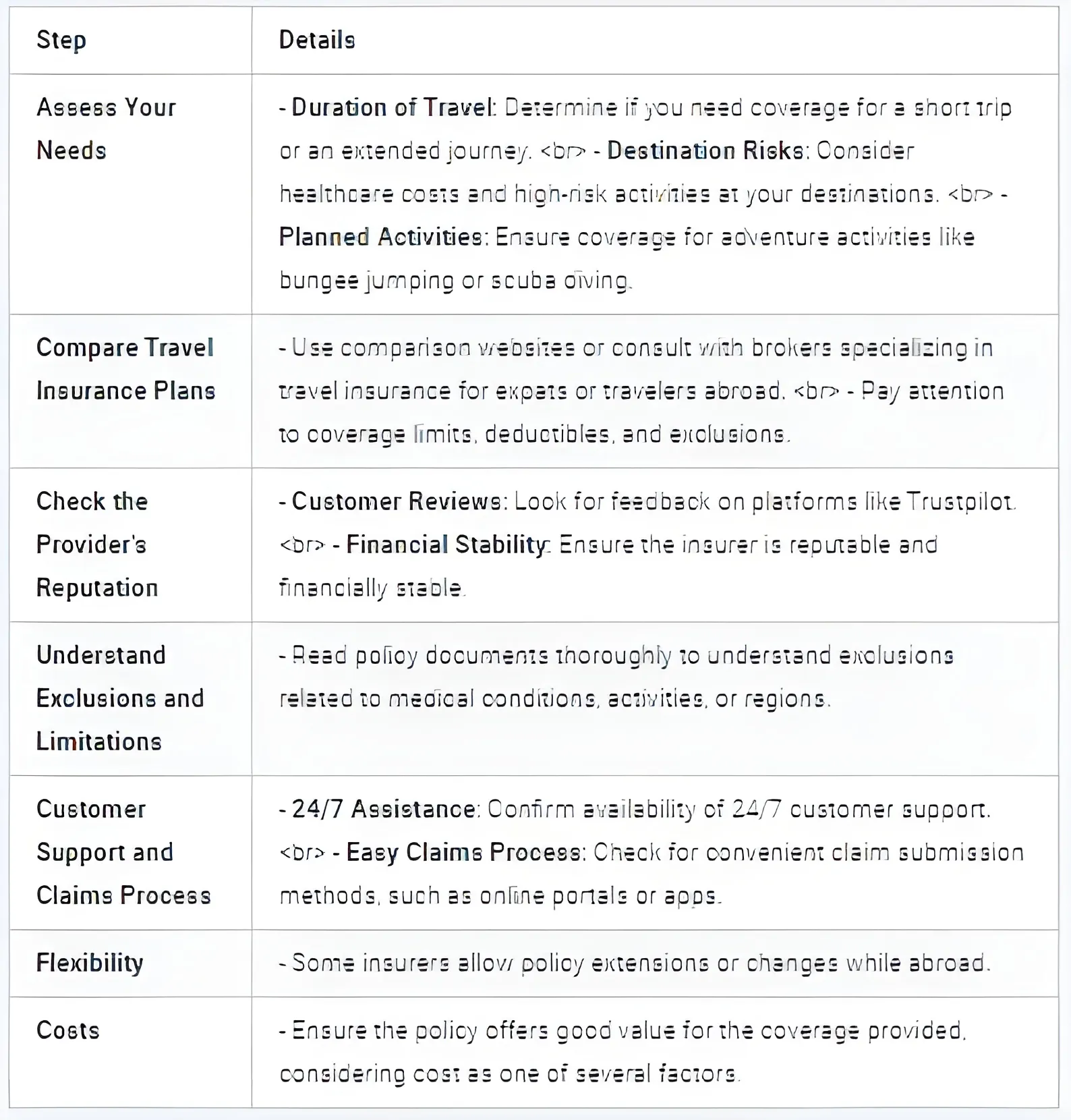

- Assess Your Needs

- Duration of Travel: Are you on a short trip or an extended journey? Some policies are better for single trips, while others cater to long-term travelers or digital nomads.

- Destination Risks: Consider the risks of your destinations, such as high healthcare costs or high-risk activities.

- Planned Activities: If you’re doing adventure activities like bungee jumping or scuba diving, ensure your policy covers them.

- Compare Travel Insurance Plans

- Use comparison websites or consult with insurance brokers specializing in travel insurance for expats or travelers abroad.

- Pay attention to coverage limits, deductibles, and exclusions.

- Check the Provider’s Reputation

- Customer Reviews: Look for feedback from other travelers. Websites like Trustpilot or consumer forums offer insights.

- Financial Stability: Ensure the insurance company is reputable and financially stable to honor claims.

- Understand Exclusions and Limitations

- Read the policy documents thoroughly. Exclusions might include certain medical conditions, activities, or regions (e.g., countries with travel advisories).

- Customer Support and Claims Process

- 24/7 Assistance: Confirm that the insurer provides 24/7 customer support, especially for emergencies.

- Easy Claims Process: Check how claims are submitted and processed. An online portal or app can make this more convenient.

- Flexibility

- Some insurers allow you to extend your coverage or make changes to your policy while abroad.

- Costs

- While cost shouldn’t be your only consideration, ensure the policy offers good value for the coverage provided.

Example:

Sarah, a digital nomad from Canada, was traveling through Southeast Asia for six months. She realized her original travel insurance was about to expire and needed a new policy. She chose a flexible travel insurance plan with monthly payments and adjustable coverage. The plan provided comprehensive medical coverage, including emergency evacuation, and covered her adventure activities such as rock climbing and surfing.

Additional Tips and Resources

- Contact Your Previous Insurer

- If your travel insurance expired, check if your previous insurer allows policy extensions from abroad.

- Consider International Health Insurance

- For extended stays abroad, consider international health insurance rather than standard travel insurance.

- Understand Local Healthcare Systems

- Knowing about the medical care facilities and costs in your destination helps you appreciate the importance of adequate coverage.

- Monitor Travel Advisories

- Government websites like the U.S. Department of State or the UK’s Foreign, Commonwealth & Development Office (FCDO) provide up-to-date travel advisories.

Internal Links:

- [Read our guide on choosing international health insurance.]

- [Learn more about travel safety tips for long-term travelers.]

Conclusion

Securing travel insurance after leaving home is not only possible but essential for protecting your journey. Unexpected events can happen anytime, and without the right insurance coverage, you might face significant financial and personal challenges. Enjoy your travels worry-free by carefully researching and choosing the right insurance plan. Don’t let the lack of coverage ruin your adventure—act now to find the best travel insurance that fits your needs.

Have you ever purchased travel insurance while already overseas? Share your experiences in the comments below or reach out with questions—we’re here to help!